ICICI Bank is focussed on building and nurturing a leading, future-ready organisation with the customer at the core.

The strategic focus of the Bank during fiscal 2020 was to continue to grow its core operating profits in a risk-calibrated and granular manner. This was driven by the objective of ‘One Bank, One ROE’, that enabled synergies across businesses. Further, the principle of 'Fair to Customer, Fair to Bank' emphasising the need to deliver fair value to customers while creating value for shareholders, guides the Bank’s operations. The underlying pillars of leveraging digital, a customer-centric and service-oriented approach, simplification of processes and enhancing customer experience were factors that were common across all businesses.

Efforts aimed at delivering maximum value to customers were further strengthened during the year. A strategic focus in this regard was to extensively leverage data analytics and market intelligence to create strategies and unique value propositions across market segments. It also facilitated better targeting, resourcing, channel and product alignment, capability building and marketing and alliances. The Bank enhanced its focus on exploring customer ecosystems that offered the opportunity to provide a wide range of products and services.

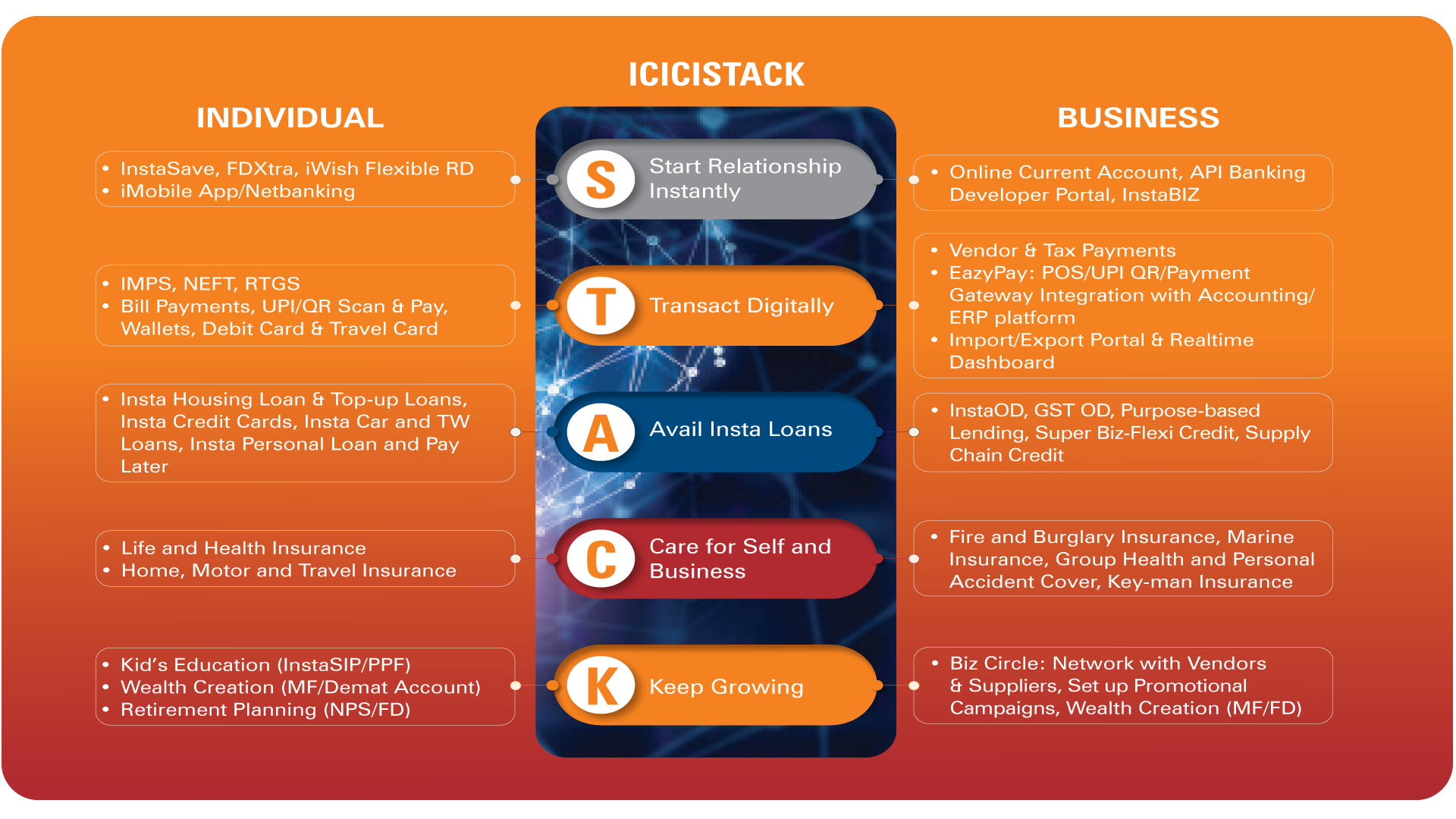

The drive to provide digital products and instant financial solutions to customers led to some unique product launches during the year that connected businesses. ICICIStack was a comprehensive digital offering launched by the Bank towards the end of fiscal 2020 that enables retail customers, retailers, professionals, fintechs, startups, e-commerce players and corporates to continue banking digitally, even from remote locations, without visiting a branch or office of the Bank. Following the outbreak of the Covid-19 pandemic, ICICIStack ensured continuity of banking services on the digital platform even during lockdown. The Bank’s application programming interface (API) banking website allows business customers to seamlessly integrate with various payment and product solutions.

KEY FINANCIAL SERVICES

Retail, Rural and SME Banking

The Bank continued to seek opportunities in the retail business space and focussed on improving its market share in segments based on the risk-calibrated profit opportunity. The retail business remained the key driver of growth with the retail loan portfolio increasing by 15.6% year-on-year at March 31, 2020. The retail loan portfolio as a proportion of the total loan portfolio increased from 60.1% at March 31, 2019 to 63.2% at March 31, 2020. Including non-fund based outstanding, the share of retail portfolio was 53.3% of the total portfolio at March 31, 2020. The Bank continued to see strong growth in its deposit base, and maintained a robust funding profile during the year. Average savings account deposits increased by 11% year-on-year and average current account deposits increased by 17.1% year-on-year. Total term deposits grew by 28.6% year-on-year.

increase in retail

loan portfolio y-o-y

increase in total

deposits y-o-y

average CASA ratio

increase in term

deposits y-o-y

Retail Banking

A customer-centric approach with a focus on maximising the lifecycle value of the relationship with the customer was a key strategy for the retail business. This involved creating digital journeys and offering a range of products from savings, investments, protection and retirement planning along with convenient payment and transaction banking services. Exploring the corporate ecosystem for opportunities in retail business was another key strategy to enable granular growth in business.

Digital sourcing of loans, both in the secured and unsecured segments grew significantly during the year. In the secured loan segment, a complete end-to-end digital solution was developed right from prospecting of customers to validating loan requests, automated underwriting, online tracking of applications and digital disbursement of funds. In the unsecured segment, efforts for improving the digital experience of customers continued which included digital underwriting processes and lending API for integration with partners and fintechs. Instant issuance of paperless and ready-to-use credit cards digitally was enabled. These cards are also enabled with security features including control features using the mobile and internet banking app. Towards the end of the year, the Bank launched a comprehensive platform, ICICIStack, that offers digital services and covers almost all banking requirements of customers including account opening, loans, credit cards, payment solutions, investments, insurance and protection related products. The platform can be used by various customer segments including retail, SME and corporate clients.

Enhancing the digital journey of customers with the Bank involved creating innovative solutions, both for customers and for relationship managers. During the year, the Bank revamped its home loan website offering an interactive customer experience and providing relevant content like calculator for checking loan eligibility, an e-book explaining the journey to purchase a home loan and a blog on the mortgage industry to enable customers to take informed decisions. For customers who are not too digitally oriented, an eRelationship Management channel was introduced, that caters to the transactions and product needs of customers through human interface on the phone. The objective is to encourage digital behaviour in customers by providing end-to-end support on the phone.

Customer Touchpoints at March 31, 2020

Branches and ATMs

Insta-banking kiosks

Cash acceptance machines

Business Correspondents

POS machines (ICICI Merchant Services Pvt Ltd.)

Simplification of processes and ensuring convenience to customers was an ongoing effort through the year. Digital onboarding of customers for opening accounts, processing service requests without human intervention, using cognitive tools for cheque clearing and encouraging paperless customer communication were a few of the key areas of focus. During the year, the Bank revamped its savings account onboarding process and enhanced system-driven validations to enable real-time account opening and activation. Features such as allowing quick fund transfer within certain limits without going through the payee registration process were enabled on the mobile app and internet banking.

Exploring opportunities through partnerships with platforms with large customer bases and transaction volumes continued during the year. The Bank launched a range of travel cards under such partnerships during the year.

The branch network was expanded with 450 new branches added during the year. The total branch network of the Bank at March 31, 2020 was 5,324. The ATM channel was further leveraged by offering services like cardless withdrawals from ATMs and creating cross-sell opportunities through the channel. The Bank added 471 insta-banking kiosks during fiscal 2020 taking the total count to 1,638 at March 31, 2020.

Rural and Inclusive Banking

The Bank’s rural banking operations cater to the financial requirements of customers in rural and semi-urban locations, primarily engaged in agriculture and allied activities. The Bank believes that the needs and expectations of rural customers are distinct from other customer segments. The Bank’s reach in rural areas comprises a network of branches, ATMs and field staff, and Business Correspondents providing last-mile access in remote areas. Of the Bank’s network of 5,324 branches, 50% are in rural and semi-urban areas with 650 branches in villages that were previously unbanked. The Bank had over 4,000 customer service points enabled through the Business Correspondent network at March 31, 2020.

The rural strategy has focussed on serving rural value chains by leveraging opportunities in different ecosystems within the rural markets. At the heart of this approach were four main ecosystems identified in the rural market which included the agriculture value chain, rural corporates, the government and the microfinance business. The Bank has developed different products and services taking into consideration the needs of every participant and leveraging banking opportunities across the business activity.

The agriculture ecosystem includes participants like seed producers, agri-input dealers, farmers, warehouses, agri-equipment dealers, commodity traders and millers. The Bank has designed different products for each player to meet their specific financial requirements so that the entire agri-value chain is well financed. Farmer financing is the primary focus within this ecosystem with products like working capital loans through the Kisan Credit Card and gold loans, and term loans for farm equipment, dairy livestock purchase and farm development. The ecosystem of rural corporates includes manufacturing and processing units, employees, dealers and suppliers who may be present in different geographies across rural India. The government network comprises of government offices, employees and institutions that implement various government schemes. The Bank closely engages with them to develop products and processes, including technology solutions. The micro-lending space includes women from the lower strata of the population, non-government organisations and other institutions working at the grassroot level in the rural economy. The Bank has products and services specifically to cater to this segment.

Apart from direct lending to customers, the Bank also engages with Microfinance Institutions (MFIs) as a crucial delivery channel in reaching out to the otherwise under-served segments of the population and enabling financial inclusion. The Bank provides financial assistance to the MFIs in the form of term loans. These funds are then further extended for on-lending to individuals and also to members of self-help groups (SHGs) and joint liability groups (JLGs) while complementing the Bank’s direct outreach to such groups.

As in all businesses, digitisation underpinned the efforts in rural banking which involved simplifying processes and empowering teams. The Bank has a mobile application which enables its employees to capture and submit loan applications from the applicant’s doorstep and also gives indicative eligibility and deviations on product lending norms. This effectively shortens the turnaround time and cost to service new loan applications. The Bank also has tie-ups with fintechs to extend its banking services to wider and deeper geographies.

Activity on the Bank’s unique mobile application for rural customers, Mera iMobile, which allows rural customers to avail over 135 services including non-banking information and agri-related advisory on crop prices, news and weather, continued to grow. The app is available in English and 11 vernacular languages, and is used by more than half a million customers. During fiscal 2020, the app had processed a total of 16.8 million financial and non-financial transactions.

The Bank has also partnered with fintech companies that support Aadhaar-enabled transactions to widen and deepen the Bank’s services across geographies. These startups facilitate cashless and paperless transactions for making payments and account transaction. During the year, 30.0 million Aadhaar-enabled transactions aggregating to about 90.00 billion were facilitated through these tie-ups.

of ICICI Bank's branches are in rural and semi-urban areas.

transactions processed on Mera iMobile in fiscal 2020.

Small and Medium Enterprises and Business Banking

The small and medium enterprises (SME) portfolio comprises exposures to companies with a turnover of up to `2.50 billion. The business banking portfolio comprises small business customers with an average loan ticket size of `10.0-15.0 million. The Bank's focus in these businesses is on parameterised and programme-based lending, which is granular and well-collateralised.

ICICI Bank offers its SME and business banking customers a wide spectrum of solutions addressing their evolving business needs such as customised offerings, faster turnaround time, transaction convenience, timely access to capital and cross-border trade and foreign exchange products. Providing digital solutions is at the core of the engagement, with the range of solutions spanning customer onboarding, payments and collections, lending and cross-border transactions.

The Bank has developed several products and solutions with digital as the medium to create value for the SME and business banking segment. In the area of customer onboarding, digital current account opening has been enabled leading to speedy account activation. A wide range of lending solutions have been developed which are offered digitally without the need to visit a branch or submit physical documents. The Bank has also enabled online electronic franking and digital signature based document execution to ensure faster processing. Customers can avail secured overdraft line of credit up to `20.0 million based on their Goods and Services Tax (GST) returns and without the need to submit financial statements.

A new digital platform, InstaBIZ, specifically for the SME and the self-employed segment, was launched during the year, which offers over 115 products and services on mobile and internet banking platforms. Customers can seamlessly execute their trade finance and foreign exchange transactions through the Trade Online and FXOnline platforms which provides a superior transaction and service experience.

During the year, a new product, Flexi-credit, was introduced for businesses. Compared to the traditional method of assessing credit eligibility based on an individual borrower’s cash flows and collaterals, this product allows customers to consolidate the cash flows of the borrower and co-borrowers and the collateral properties of the borrower and the co-borrowers for evaluating the credit eligibility of the borrower.

Supply chain financing is an integral part of the SME business and a focus area towards deepening the Bank’s coverage of the corporate ecosystem. The SME group provides seamless and fast access to finance to dealers and vendors of a corporate customer along with meeting their regular banking requirements both at the business entity and personal banking level. The Bank has developed an integrated supply chain system that can be integrated with the corporate’s Enterprise Resource Planning (ERP) for seamless collection from dealers and payment to vendors. The system provides real-time reconciliation and reports to the corporate. It also enables the Bank to provide channel finance based on the transaction flow and payment track record. The Bank has also launched a non-ERP version of the dealer finance solution which is fully digitised end-to-end.

The Bank follows strong risk management practices in managing its SME and business banking portfolio, with a view to enhancing the portfolio quality by reducing concentration risk and a focus towards granular and collateralised-lending based growth. Robust monitoring frameworks have been put in place for transaction-based review and proactive and early action is taken to ensure healthy portfolio quality. The risk assessment of SME customers was enhanced during the year. The Bank has adopted a streamlined underwriting process using digital tools like bank statement analyser, automatic fetching of bureau reports and business rule engine to generate probability of default scores for score-based analysis. A combination of qualitative and quantitative assessment tools are used to arrive at the final decision.

With a view to increase the risk adjusted operating profit from the portfolio and enhance the return on equity, reliance is also placed on harnessing opportunities across transaction banking, foreign exchange and personal banking solutions with the SMEs.

Wholesale Banking

The Wholesale Banking Group has a deep customer franchise which includes top business houses, large private sector companies, financial institutions and banks, public sector undertakings, and government departments and entities. In the last few years, the team has developed a very strong franchise across MNCs and new-age services companies. The team has also established a franchise in the financial sponsors space with special focus on private equity funds and their investee companies.

The Bank has a strong presence across the country which enables it to service corporate clients with ease and speed. Over 100 dedicated Transaction Banking branches have been identified for prompt servicing of corporate transactions. For meeting the foreign exchange and derivative requirements, the Wholesale Banking Group is supported by one of the largest treasuries in the country. The leading edge product portfolio is comprehensive and technologically-advanced and includes lending products for working capital and capital expenditure requirements and other products that the client may need across trade, treasury, bonds, commercial papers, channel financing, supply chain solutions, and various other activities.

A key theme during fiscal 2020 was to deepen the customer-centricity approach in the Bank’s product offerings and to use digital channels for service delivery. For the Wholesale Banking Group, the underlying theme followed was 'Ecosystem Banking for a Corporate' wherein the corporate relationship manager services a corporate and its entire network of employees, dealers, vendors and all stakeholders with a complete suite of banking products. This strategic focus enabled the team to penetrate deeper in high value retail accounts of corporate owners and employees through a suite of retail products like salary, private and wealth banking, home loans, personal loans, vehicle loans, etc. Apart from being a single-point solution provider, this approach also reduces customer acquisition cost. The team also focussed on capturing the customer flows in its ecosystem to strengthen the liability franchise further.

In a volatile business environment, with return of capital being the overarching objective, the Wholesale Banking Group leveraged analytics extensively to monitor transactions and portfolio quality. While new credit is extended in a granular manner to well-established and higher rated business groups, analytics was used for portfolio monitoring and identification of early warning signals in the existing book. This led to enhancement of quality of the existing corporate portfolio. The team also focussed on reducing concentration risks to make the portfolio more granular. Another significant achievement on the digital front was the launch of an online application for credit assessment of mid-corporate clients. This will enable objective and comprehensive risk assessment of clients based on multiple parameters like bureau information, qualitative and quantitative factors, and also help the team in adopting a consistent approach to onboarding of clients as well.

Transaction Banking

Transaction banking is an important value proposition for corporates for the day-to-day functioning of their businesses which includes account services, payment and collection services, domestic and cross-border trade finance, working capital finance and supply chain finance. Transaction banking services are delivered through the network of branches across the country including 107 specialised branches which are enabled to meet the specific needs of the corporate customers and a team of account managers. The products and services are also delivered through the Bank's Corporate Internet Banking (CIB) platform and also through its mobile application InstaBIZ. These digital applications cater to a significant proportion of the overall transaction volume.

Transaction banking offers integrated cash management and trade finance solutions to the customers. By integrating the Bank’s system with their Enterprise Resource Planning (ERP), the customers are able to process their collection and payments digitally including seamless reconciliation and accounting. The digitisation of the export and import data by the Reserve Bank of India has been leveraged to offer digitised trade finance solutions including paperless imports and export processing of transactions. This facilitates faster delivery of products and services to the customers.

Advancements in technology have enabled the Bank to reimagine various customer journeys and create industry-specific solutions. These solutions not only digitise and thereby simplify processes, but also help customers to digitise their entire ecosystem which includes their vendors, partners and customers. Some of the solutions include an application for software exporters that helps process almost 10% of the IT/ITeS exports of the country, and a first-to-market platform to digitise procurement through e-tendering. The e-tendering solution is aiding over 4,000 units to seamlessly integrate their complex procurement workflows. The Bank also developed specific solutions for commodity board ecosystems through its Digi-Commodity offering. This platform enables digital collection of auction proceeds and auto reconciliation of outstanding invoices, all the while allowing for deal-wise settlement across multiple stakeholders. More than 8,000 stakeholders are regularly using this platform.

The Bank has also entered into partnerships, especially with fintechs, to enhance the customer proposition. Some of these partnerships are in the area of supply chain finance and specialised ERP service providers.

The Bank launched iXpress Connect, a portal that hosts standard API protocols enabling corporate clients to seamlessly access the Bank through APIs.

The Digi-Commodity platform enables digital collection of auction proceeds and auto reconciliation of outstanding invoices, while allowing for dealwise settlement across multiple stakeholders.

Another area is API Banking that is also playing an important role in shaping the Bank’s strategy. The Bank has a developer portal wherein 250 API services are available for customers. The Bank is also considering an advanced API portal which can cater to more complex workflow requirements. Similarly, blockchain-based solutions have been implemented by the Bank in the area of trade finance which has significantly added value to all stakeholders and is now being made into an industry-wide initiative along with other banks.

The Bank has leveraged analytics to enhance customer experience, manage risks and better service delivery. The Bank believes that investments and strategic initiatives undertaken would enable it to deliver industry-leading services to customers and build a stable franchise for the Bank.

International Business

ICICI Bank’s international presence consists of branches in the United States, Singapore, Bahrain, Hong Kong, Dubai International Finance Centre, China, Offshore Banking Unit (OBU) and IFSC Banking Unit (IBU). The Bank also has wholly-owned subsidiaries in the United Kingdom (UK) and Canada with branches across both countries. ICICI Bank UK also has a branch in Germany.

The Bank has repositioned its international franchise to focus on non-resident Indians (NRIs) for deposits, wealth and remittances businesses. The Bank is also focussed on deepening its relationships with Indian corporates in international markets and multinational companies present in international as well as domestic market, for maximising the India-linked trade, transaction banking and lending opportunities. The Bank is also actively engaging with sovereign wealth funds, global pension funds and asset managers to facilitate fund flows into India. The Bank also aims to reduce exposures that are not linked to India in line with the focus on growing the India-linked business.

The Bank has repositioned its international franchise to focus on NRIs for deposits, wealth and remittances businesses.

The Bank continues to play a pioneering role in promoting digital initiatives across businesses in the international banking arena and has been continuously introducing and innovating products to enhance customer experience. In the remittances space, the Bank introduced online inward remittance facility for low value commercial transactions. Blockchain based processing for outward remittances was extended to the UK and Europe corridors, besides Canada. Further, digital platforms were launched for facilitating fee payments by students.

To meet the banking needs of NRI customers, a complete revamp of both the product and service proposition was undertaken during the year. For NRIs in Canada and the UK, a fully digital account opening solution was launched to enable them to have a global view of their accounts in their home country and India. Other digital solutions, including ICICIStack, are proposed to be introduced in international markets in the near term.

Government Banking

The Bank considers the government to be an integral partner that facilitates large scale investments in the economy and requires comprehensive support in terms of services and banking solutions. The Bank engages with the government departments and bodies across various levels, at central, state, district and local bodies including municipalities and gram panchayats. The products and services offered are not only financially-oriented, but are also enabling solutions for enhancing e-governance through IT solutions, integrated collections and payment solutions facilitating participation in pilot projects. These efforts also result in deposit balances for the Bank. The Bank has also partnered with the governments and local bodies during periods of disaster and crisis.

With the philosophy of 'Fair to Customer, Fair to Bank', the Bank will continue to diligently and efficiently service all its clients and create value for their enterprises as well as for the Bank.

CUSTOMER SERVICE

Understanding customer expectations and responding through appropriate products and services has been central to the Bank’s strategy. The demand for convenience, speed and customised solutions with quick turnaround and innovative solutions requires a dynamic culture in the Bank. The concept of customer satisfaction has now been replaced by ‘delight’ in banking experience. The Bank has embraced and built upon this transition while being committed to the core principle of 'Fair to Customer, Fair to Bank'.

During fiscal 2020, mapping of customer journeys across products, processes and channels was undertaken and based on the insights, key customer service initiatives were implemented. The key initiatives during the year were in the areas of account opening, servicing, NRI customer experience, process simplification, and technology platform and system upgradation. Some of these initiatives were:

- The account opening process was simplified for savings and current accounts

- Digital communication and status dashboards were launched for mortgage customers and internal stakeholders enabling stage-wise tracking of loan applications

- A simplified and widgetised dashboard and user interface was launched for retail and corporate internet banking customers

- Digital signing and stamping of documents was enabled for corporate, SME and business banking customers

- The NRI account opening experience was enhanced through simplification of the account opening form and implementation of Optical Character Recognition (OCR) to reduce customer effort. A dedicated NRI Expert Team (NET) was set up for enhanced NRI servicing

- An integrated new platform for processing trade transactions was deployed

During the year, there was sustained improvement in the Net Promoter Score (NPS), a key metric for measuring customer advocacy for onboarding, branch and digital channels.

The Bank ensures continuous engagement with its customers through multiple channels including branch employees, surveys, social media and channels for raising queries and grievances.

The Bank has a well-defined framework to monitor key customer service metrics. The Customer Service Committee of the Board and the Standing Committee on Customer Service meet on a regular basis. These forums deliberate on issues faced by the customers and the initiatives taken by the Bank for enhancing customer service.

The Bank complies with the 'Customer Rights Policy' which enshrines the basic rights of customers of the Bank. These rights include Right to Fair Treatment; Right to Transparency, Fair and Honest Dealing; Right to Suitability; Right to Privacy and Right to Grievance Redress and Compensation.

Customer Grievance Redressal Mechanism

The Bank seeks to treat its customers fairly and provide transparency in its product and service offerings. The Bank makes continuous efforts to educate its customers to enable them to make informed choices regarding banking products and services. The Bank also seeks to ensure that the products offered are based on an assessment of the customer’s financial needs.

The Bank has a well-defined grievance redressal mechanism with clear turnaround times for providing resolution to customers. All complaints received by the Bank are recorded in a Customer Relationship Management (CRM) system and tracked for end-to-end resolution. The Bank also has an escalation matrix built in the CRM system to ensure that customer requirements are appropriately addressed within stipulated timelines. Further, as recommended by the Reserve Bank of India, the Bank has appointed a senior retired banker as the Internal Ombudsman of the Bank. The Customer Service Committee of the Board, the Standing Committee on Customer Service and the Branch Level Customer Service Committees monitor customer service at different levels.

For details on customer complaints, please click here

TECHNOLOGY FOCUS

The Bank’s technology initiatives are aimed at enhancing value and offering customers greater convenience and improved service levels while optimising costs. The Bank continues to invest in key technological areas like mobility, cognitive intelligence, blockchain, natural language processing, machine learning, API banking, micro-services, cloud, ecosystem synergies, Robotics Process Automation (RPA) and other new-age technologies that provide an edge to the Bank’s offerings to its customers and deliver its strategic objectives.

The technology strategy is based on the following set of guiding principles:- Superior customer convenience

- Alignment of technology to business strategy

- Flexible and modular IT infrastructure that enables inter-operability

- Adoption of emerging technologies to facilitate innovation

- Collaborative approach to providing solutions across all stakeholders

- Optimisation of processes and superior decisioning by simplification and use of data

In order to deliver the overall business objectives and make Information Technology as an enabler, the Bank has defined a four-pronged strategy.

Focus on Data, Fintechs, APIs and Ecosystems

The Bank has a dedicated Data Science and Analytics team that works across business areas on projects relating to business analytics, decision strategies, forecasting models, machine learning, rule engines and performance monitoring. The Bank maintains a comprehensive enterprise-wide data warehouse and employs statistical and modelling tools for leading-edge analytics.

In driving an innovation and startup mindset, the Bank has set up an Innovation Centre to collaborate with and invest in fintech startups and co-develop products aligned with the ICICI Group’s digital roadmap. The engagements with the startups are focussed on digital lending, revenue growth, digital platforms and process efficiencies.

While the Bank is focussed on growing its own digital channels, it is also creating an ecosystem through partnerships which cover all broad segments of customer and merchant payments. The Bank is offering a host of APIs and SDKs (software developer kits) which facilitate third-party apps to offer payment solutions for their retail customers.

The Bank has launched an API Banking portal which consists of 250 APIs and enables partner companies to co-create innovative solutions in a frictionless manner and in a fraction of the time usually taken for such integration.

RESPONSIBLE BANKING

The Bank is committed to act professionally, fairly and with integrity in all its dealings. It has a zero tolerance approach to bribery and corruption and has a well-defined policy articulating the obligations of employees in these matters. The responsible banking pillars also include a focus on cyber security and data privacy.

Cyber Security

ICICI Bank believes that cyber security is an important risk focus considering the rapid digitisation, increasing transaction intensity and connectivity to networks and ecosystems. It is vital to protect the Bank’s and customers’ assets and ensure continued trust of all stakeholders. ICICI Bank has adopted a multi-dimensional approach to cyber security. The CIA triad of confidentiality, integrity, and availability is at the heart of the information security framework implemented by the Bank. Keeping customer priorities in mind, the Bank follows a ‘defence-in-depth’ approach in implementing cyber security solutions. This approach enables the Bank to protect its data using a multi-layered defence mechanism using a combination of tools and techniques which complement and augment each other.

The Bank also lays emphasis on customer elements like protection from phishing, adaptive authentication, awareness initiatives and above all easy-to-use protection and risk configuration ability in the hands of the customers. Customer-facing applications are designed with the aim to provide consolidated customer information in a safe and secure manner. The Bank has given its customers complete control on card options like online usage, international transaction capability and others on its mobile app and internet banking platform. This gives customers control on card safety on a real-time basis.

The Bank has formulated robust security standards, processes and protocols which are proactively reviewed and enhanced in the backdrop of an ever-evolving cyber security landscape. The Bank has developed a comprehensive framework and policy which includes the Information Security Policy, Cyber Security Policy and Cyber Crisis Management Plan to ensure adequate security of assets on a continuous basis. The governance structure for management of information and cyber security risk is helmed by Board-level Committees including the IT Strategy Committee, the Risk Committee and Audit Committee. In addition, there are also specialised committees to review areas of IT and cyber risk, like the Information and Cyber Security Committee. Additionally, the Bank has devised multiple key risk indicators and dashboard to keep a track of system stability, continuity and availability, and network uptime.

The Bank ensures 24x7 monitoring and surveillance of systems through its Security Operations Centre. The Bank has a fully equipped disaster recovery set-up in place at remote locations, which is supplemented by periodic disaster recovery drills. Further, stringent gating controls are followed at the time of induction of new applications. Based on the changing threat landscape, the Bank has procured a Cyber Insurance Policy which is reviewed and renewed every year and new risk areas are included if deemed necessary. Considering data protection is critical, a Data Leakage/Loss Prevention (DLP) system is in place in order to protect confidential data at endpoint, network and storage levels. The Bank also has an in-house ethical hacking team (red teams) to continuously test banking applications for vulnerabilities or security flaws. Also, the Bank undergoes multiple assessments of its security by internal as well as external auditors, through specific thematic assignments and regulators to continuously check its security approach and strengthen its controls.

The Bank also conducts and participates in cyber security drills to continuously fine tune its response mechanisms. The Bank also runs frequent awareness campaigns for employees through mailers, screen savers, etc., and conducts internal simulation exercises to ensure high levels of employee awareness on information security.

In the wake of the Covid-19 outbreak, and banking being classified as an essential service, the Bank made arrangements for several key activities to be performed through secure work-from-home (WFH) technology solutions. While rolling out these solutions, appropriate controls have also been implemented for information security. Further, detailed advisories have been issued on Dos and Don’ts for employees to follow when they work from home. This is also being followed up with regular communication on information security best practices. Additional monitoring parameters have also been configured on the Bank’s 24x7 Security Operations Centre to continually monitor logs pertaining to WFH access of employees and generate alerts in case of any unusual events.

There were no material incidents of security breaches or data loss during fiscal 2020.

Data Protection and Privacy

ICICI Bank is committed to protecting the privacy of individuals whose personal data it holds, and processing such personal data in a way that is consistent with applicable laws. It is important for employees and businesses to protect customer data and follow the applicable privacy laws to ensure safety and security of data. The Bank believes that the data privacy framework should be robust and in line with the evolving regulatory changes and digital transformation.

ICICI Bank has a global presence in several overseas jurisdictions including Hong Kong, Singapore, US, UK, Canada, China, Dubai International Financial Centre and Bahrain. It becomes very important for the Bank to have an integrated and centralised strategy for achieving data privacy compliance. A set of principles have been defined with respect to handling customer data. There is also a mechanism in place for reporting any form of data breach.

On account of the changes in data protection laws and regulations, in fiscal 2020 the Bank updated its Personal Data Protection Standard to cover the personal data protection regulatory requirements of overseas jurisdictions to the extent that those regulations are applicable to the Bank. Privacy regulations require personal data of the customers to be protected throughout its entire lifecycle. Accordingly, the Bank has undertaken several comprehensive measures such as categorising all Personal Data and Sensitive Personal Data as ‘Confidential Information’, maintaining a record of all its processing activities, entering into non-disclosure and confidentiality agreements with its employees and third parties who are privy to personal data of the customers, providing customers options to exercise the rights which they enjoy under applicable data protection regulations, incident handling procedures, etc. Various data privacy awareness initiatives and periodic trainings have been undertaken. ICICI Bank is steadfast in its commitment to protect the privacy of its customers.

KEY PRODUCTS INTRODUCED IN FISCAL 2020

ICICISTACK

This is the most comprehensive digital infrastructure available in the banking industry which enables millions of retail customers, merchants, retailers, professionals, fintechs, startups, e-commerce players and corporates to continue uninterrupted banking services digitally, without visiting any bank branch. ICICIStack offers nearly 500 services that cover almost all banking requirements of customers in one place. The list includes digital account opening, loan solutions, payment solutions, investments and insurance solutions. Even non-customers of the Bank can get the benefit of ICICIStack easily by simply opening an instant savings account with the Bank digitally. A business entity, in case it is a not a customer of the Bank, can download the InstaBIZ app which is specially curated for businesses, and enjoy the unparalleled convenience of ICICIStack. Additionally, business entities can get access to easy bulk collection and payments of funds through multiple digital modes, automatic bank reconciliation and can undertake most of the export-import transactions including inward and outward remittances digitally.

API BANKING

ICICI Bank launched India’s largest and fully digital API (Application Programming Interface) Banking portal enabling partners to integrate various payment and product solutions in a few days. The process is frictionless and much faster than the time usually taken for such integration, thereby significantly increasing the productivity of partners. The portal consists of 250 APIs, the maximum number of virtual APIs put together by any Indian bank. The APIs are available across an array of categories including payments & collections like IMPS, UPI payment/collection accounts & deposits, and cards & loans.

WHATSAPP BANKING

ICICI Bank launched WhatsApp Banking to enable retail customers to undertake a slew of banking requirements from their home at a time when they are advised to stay indoors in the wake of the Covid-19 outbreak. Using the WhatsApp Banking service, customers can check their savings account balance, last three transactions, credit card limit, get details of pre-approved instant loan offers and block/unblock credit and debit card in a secure manner with end-to-end encryption for all messages. They can also get details of the three nearest ATMs and branches of ICICI Bank in their vicinity.

INSTABIZ

InstaBIZ is the country’s first comprehensive and only digital banking platform for self-employed segment and MSMEs. It provides a bouquet of comprehensive solutions in ‘one single place’. It allows customers to avail over 115 products and services in a digital and secure manner. The range of services available on InstaBIZ include instant overdraft facility (up to `1.5 million) and business loans, easy bulk collection and payments of funds through multiple digital modes and automatic bank reconciliation. Further, it is the first digital banking platform to enable instant payment of GST using the challan number in a single click payment. Additionally, customers can instantly apply for a Point-of-Sale (PoS) machine as well as instant marine insurance policy. The customers can access the services of InstaBIZ on their mobile phone and on the Bank’s internet banking platform. MSMEs, who are not customers of the Bank, can also download InstaBIZ and enjoy the un-paralleled convenience of industry-first solutions.

CARDLESS CASH WITHDRAWAL

The Bank launched the Cardless Cash Withdrawal facility which allows customers to withdraw cash from its ATMs without using the debit card. The customers can withdraw cash from over 15,000 ATMs of the Bank by simply raising a request on the mobile banking app, iMobile. It can be used by customers themselves when they do not wish to carry the debit card. The daily transaction limit as well as per transaction limit is set at `20,000 for this facility.

iBOX

This is a unique self-service delivery facility, enabling customers to collect their deliverables such as debit card, credit card, cheque book and returned cheques, from a branch close to their home or office, in a hassle-free manner. The Bank has introduced this facility at over 50 branches in 17 cities in the country. The fully automated process informs the customer of the current status of their package, from despatch to delivery, via an SMS at every stage.

SMART EMI

Launched in association with TranzLease, an automobile leasing and mobility solutions company, SMART EMI is the next-gen auto loan facility that enables customers to drive a new car home at lower cost and higher convenience. Under this facility, the amount of EMI paid is much lower than a regular car loan as the estimated resale value of the car is deducted upfront. The customers also have an option to either own the car at the end of the tenure by paying an agreed resale value or simply returning the car to the leasing company. In case of such return, customers are rewarded with special bonus. Also, the facility takes care of the insurance and maintenance requirements of the vehicle during the financing period.

iXPRESS CONNECT

ICICI Bank launched iXpress Connect, a portal that enables its corporate clients to remotely design, develop, test, use and integrate their systems with the Bank through APIs. iXpress Connect showcases all hosted APIs to the customers so that they can select the relevant API for their business needs. Clients can access the portal anytime, from anywhere and are not dependent on the Bank for API development and configuration. iXpress Connect helps create a unique customised experience for each client in accessing the Bank through APIs.

FD HEALTH

This Fixed Deposit (FD) offers dual benefits of investment growth via FD and protection through critical illness coverage. Customers opting for this fixed deposit also get a complimentary critical illness cover of `100,000 from ICICI Lombard General Insurance Company on opening an FD of `200,000 to `300,000 for a tenure of at least two years. The customers in the age bracket of 18 to 50 years get a complimentary insurance cover for a year on 33 critical illnesses.