Offers

Offers

Grow Investment

Grow Investment

Customer Care No.

Customer Care No.

Offers for you!!

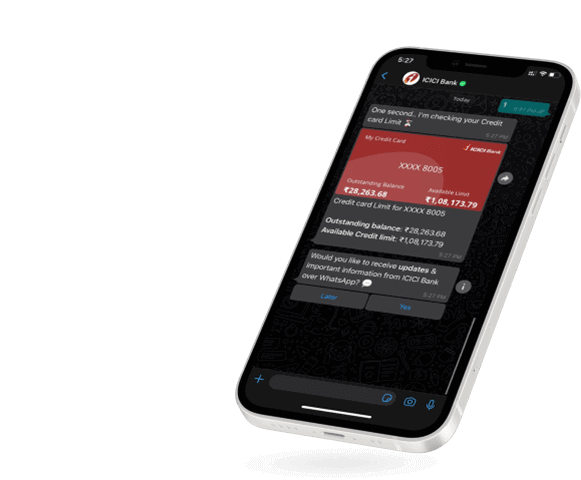

.png)

Grow your Investment

For any banking assistance, please call our customer care number.

![]()

![]() 1800 1080

1800 1080

Platinum Chip Credit Card

- No Joining Fee. No Annual Fee

- Earn ICICI Bank Rewards Points on your spends except fuel

- Exclusive Dinning Offers through Culinary Treats Programme

- Save on 1% fuel surcharge, waived off at HPCL petrol pumps

Coral Credit Card

- Joining fee 500 + GST

- Earn up to 10,000 additional reward points

- Buy 1, get 1 movie ticket free at BookMyShow

- One complimentary railway lounge visit per quarter

Rubyx Credit Card

- Exclusive privileges - entertainment, dining, wellness and golf

- Complimentary airport lounge access

- Buy 1, get 1 movie ticket free at BookMyShow

- Welcome Vouchers on Shopping and Travel worth Rs 5000

Sapphiro Credit Card

- Exclusive privileges - entertainment, dining, wellness and golf

- Complimentary membership to the Dreamfolks DragonPass programme

- Buy 1, get 1 movie ticket free at BookMyShow

- Welcome Vouchers on Shopping and Travel worth Rs 10,000

abc

PL

Get a call back to know best offer on credit cards

MakeMyTrip ICICI Bank Platinum Credit Card

- Joining Fee- Rs 500 + GST

- Rs 500 My Cash plus MakeMyTrip holiday voucher worth Rs 3,000 on joining

- Enjoy complimentary domestic airport & domestic railway lounge access

- Get an extended validity of 1.5 years^ on Joining Benefit My Cash

MakeMyTrip ICICI Bank Signature Credit Card

- Joining Fee- Rs. 2,500 + GST*

- Rs. 1,500 My Cash* plus MakeMyTrip holiday voucher worth Rs 2,500 on joining

- complimentary MMTBLACK Exclusive membership

- Enjoy complimentary international and domestic airport lounge access and domestic railway lounge access

- Get an extended validity of 1.5 years^ on Joining Benefit My Cash

(*Joining benefits will not be applicable for lifetime free cards)

MakeMyTrip ICICI Bank Signature Credit Card

- Joining Fee- Rs. 2,500 + GST*

- Rs. 1,500 My Cash* plus MakeMyTrip holiday voucher worth Rs 2,500 on joining

- complimentary MMTBLACK Exclusive membership

- Enjoy complimentary international and domestic airport lounge access and domestic railway lounge access

- Get an extended validity of 1.5 years^ on Joining Benefit My Cash

(*Joining benefits will not be applicable for lifetime free cards)

MakeMyTrip ICICI Bank Signature Credit Card

- Joining Fee- Rs. 2,500 + GST*

- Rs. 1,500 My Cash* plus MakeMyTrip holiday voucher worth Rs 2,500 on joining

- complimentary MMTBLACK Exclusive membership

- Enjoy complimentary international and domestic airport lounge access and domestic railway lounge access

- Get an extended validity of 1.5 years^ on Joining Benefit My Cash

(*Joining benefits will not be applicable for lifetime free cards)

abc

PL

Get a call back to know best offer on credit cards

Manchester United Platinum Credit Card

- Joining Fee - Rs 499 + GST

- Get a Manchester United branded football on activation

- Top 20 Spenders: Get a Manchester United Branded Merchandise Kit*

- 1 complimentary domestic airport lounge visit per quarter

Manchester United Signature Credit Card

- Joining Fee- Rs 2,499 + GST

- Get a Manchester United branded holdall and football on joining

- Top 20 Spenders: Get a Manchester United Branded Merchandise Kit*

- 2 complimentary domestic airport lounge visits per quarter

Manchester United Signature Credit Card

- Joining Fee- Rs 2,499 + GST

- Get a Manchester United branded holdall and football on joining

- Top 20 Spenders: Get a Manchester United Branded Merchandise Kit*

- 2 complimentary domestic airport lounge visits per quarter

Manchester United Signature Credit Card

- Joining Fee- Rs 2,499 + GST

- Get a Manchester United branded holdall and football on joining

- Top 20 Spenders: Get a Manchester United Branded Merchandise Kit*

- 2 complimentary domestic airport lounge visits per quarter

abc

PL

Get a call back to know best offer on credit cards

DIGITAL BANKING

Advance. Innovative. Instant

- Mobile Banking

- Net Banking

- WhatsApp Banking

DIGITAL BANKING

Advance. Innovative. Instant

Download

iMobile App

Click to Enlarge

Download

Pocket

Click to Enlarge

Exciting deals on ICICI Bank Net Banking

Explore now

We take your Banking security

seriously !

Peace of mind for you as we have the most advanced technology & protection

2 Factor i-safe authentication

End-to-end 256 bit Encryption

We make you feel special

Trending Deals

Great Offers for Great Experiences