Want us to help you with anything?

Request a Call back

Now that you have your Sanction Letter, take the final steps to get your Home Loan disbursed and have a home of your own.

Please click Track My Loan or contact your Relationship Manager.

![]() For further details, give us a missed call on 9699099411

For further details, give us a missed call on 9699099411

Disbursement Process

After your file moves ahead from the sanction and property evaluation stages, the Bank decides the final amount, which can be disbursed basis the stage of the property evaluation.

The next step is to complete the final formalities of the disbursement. In this stage, you as a customer have to sign a few agreements like Mandates, Disbursement Request Form and the Facility Agreement of the loan amount, with respect to the transaction type. The Bank also requires the original documents pertaining to the mortgage transaction to validate the collateral security.

After completing all the processes, the Bank proceeds to disburse the amount in favour of the recipient, based on the banking proofs submitted.

The customers get to decide the date of disbursement, the date of an EMI and the mode of disbursement as per their convenience.

Get Disbursement Assistance

Financial institutions apply a wide range of risk assessment tools to gauge a borrower’s creditworthiness. This task is carried out diligently in case of long-term big-ticket mortgages like Home Loans, for obvious reasons. Apart from examining the individual creditworthiness of the applicants, banks also apply several checks on the property for sale. Since this is an asset acting as a security against the Loan, no stone is left unturned to ensure that the bank is lending money towards a safe property. Thus, banks carry out a legal and technical verification of the property, for which they would grant the Loan. Once both the legal and technical parameters are met, the bank will proceed to the final stage of the Loan disbursement process.

Contact your Relationship Manager for making a choice for your dream home.

- Property Not Identified:

-

Bank approved projects refer to those properties whose title and other legal documents have been examined by the Bank thoroughly, so that interested home buyers can be assured that the project is legally clear and they can go ahead with the property purchase, without worrying about likely issues on the builder’s title/right to the property being built. Banks also inspect the building plan and all other clearances required by the builder for the construction, as a part of its project approval process.

Visit http://home.icicibank.com/home to choose your dream home.

Contact your Relationship Manager for making a choice for your dream home.

- Property Identified:

-

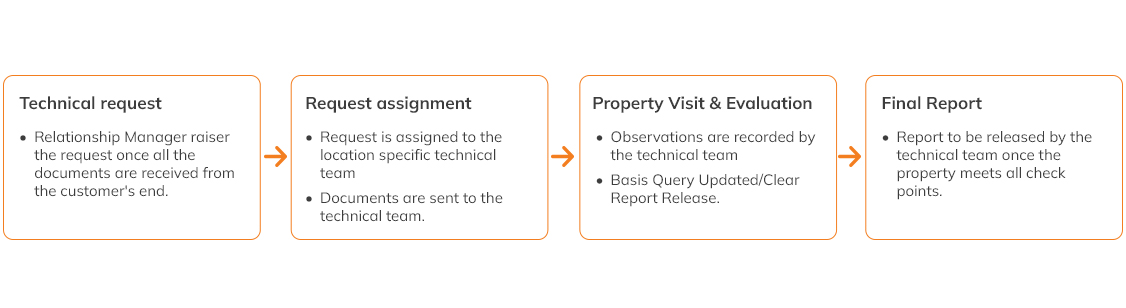

If you have already finalised your property, the next stage of the Loan disbursement is property evaluation. Property evaluation is done both legally and technically. An ICICI Bank empanelled lawyer does legal valuation. Certified property evaluators do the technical valuation.

Contact your Relationship Manager for any process support.

*In case of APF Builder Purchase cases, legal evaluation is waived off.

Contact your Relationship Manager for initiating property evaluation.

Click here to check state-wise requirements for Legal Evaluation.

Contact your Relationship Manager for initiating property evaluation.

Click here to check state wise requirements for Technical Valuation

List of documents required for disbursement of Loan

| Document category | Documents required |

|---|---|

| Facility Agreement | Duly filled and signed by all the applicants with franking(state specific) and MOE/MODT/MOD state specific will be required as applicable |

| Disbursement Request Form (DRF) | Disbursement Request Form (DRF), signed by all the applicants. |

| Repayment Mode | E-NACH or Auto Debit mandate as applicable |

| (Security E-NACH as applicable) | |

| 3 SPDC required for loan above 1 cr (One third of the loan outstanding amount) | |

| First PreEMI cheque to be provided with favoring details | |

| Most Important Information (MII) and Key Fact Sheet | Signed by all the applicants. |

| Administration Charges | Rs5000/- or 0.25 % of the loan amount whichever is lower plus applicable taxes (The Administrative charges are a one-time non-refundable charges collected by the Lender for the purpose of appraising the valuation and legal verification of property to ascertain suitability of accepting the property for mortgage and the same is independent of the outcome /result of such appraisal. Please note that the administrative charges are payable at the time of disbursement of the Facility) |

| Stamp Duty | State wise Stamp duty will be applicable |

| Notice of Intimation | Notice of Intimation (NOI) will be applicable for properties situated in Maharashtra. NOI to be done within 30 days from the first disbursement date |

| Sanction Letter | Accepted Sanction Letter, signed by all the applicants. |

| Pending documents, if any, as per the sanctioned conditions. | |

| Property Documents | Sale Deed and additional agreement, as applicable. |

| Current Agreement with Registration Receipt and Index 2, as applicable. | |

| Total linked documents. | |

| Approved plan and permissions from the appropriate authority. | |

| Copy of the latest Encumbrance Certificate (EC), as applicable. | |

| Copy of the latest Property Tax Receipt, as applicable. | |

| Click here to view State and transaction wise Property Documents list. | |

| Legal and Technical clearance to be obtained for Loan Disbursement. |

Transaction wise list of additional documents

| Transaction Type | Documents required |

|---|---|

| Resale | Seller verification. |

| Copy of PAN or Aadhaar Card, of all the sellers. | |

| 3 months Seller's Bank Statement | |

| Resale Affidavit. | |

| Bank Statement reflecting Own Contribution Receipt (OCR) Clearance. | |

| Under-construction | Bank Statement reflecting OCR Clearance. |

| Balance Transfer | Balance Transfer Drafts with franking and notary |

| Original Documents List, as on date. | |

| Pre-closure Letter of the existing bank, as on date. | |

| Original verification for BT, from the Co-Operative Bank. | |

| Land Loan/Self Construction/NRP Plot + Construction | Declaration for self-construction. |

| Lease Rental Discounting (LRD) | Facility Agreement with franking. |

| Hypothecation Deed with franking. | |

| Trust and Retention agreement. | |

| Single Composite letter for Lessor and Lessee |

After your file has passed both the sanction and property evaluation stages, the Bank decides the final amount, which can be disbursed basis the stage of property evaluation.

Hence, the next responsibility as a recipient is to finish the final formalities of the disbursement.

In this stage, you as a customer have to sign few agreements with respect to the transaction type, like Mandates, Disbursement Request Form and Facility Agreement of the Loan amount.

Along with this, Bank also requires the original documents pertaining to the mortgage transaction to validate the collateral security.

After all the processes are ticked, Bank proceeds to disburse the amount in favour of the recipient, based on the banking proof submitted.

Customer gets to decide the date of disbursement, date of EMI and mode of disbursement based on their convenience.

- Disbursement Documentation:

-

Contact your Relationship Manager for any doubts regarding the checklist.

- Seller Verification/Original Document Verification (In case of Resale/Non APF Builder Purchase)

-

Seller Verification happens in case of Resale properties. Here a bank employee verifies the identity and banking of the seller physically. This activity is done to authenticate the nature of the transaction and genuineness of the individual, using both bank’s validation (Bank Statement) and Identity Validation (PAN Card/Aadhar Card).

*All the Title Owners of the property have to co-operate for Seller Verification.

Contact your Relationship Manager to understand the applicability of the Seller Verification in your case.

- EMI Date & Pre EMI Charges (what)

-

At ICICI Bank, there is a flexibility in the choice of EMI Date i.e., 1st of the Month, 5th of the Month. Apart from these two dates, if in a rare case the customer’s salary credit is beyond 5th of the month, then 10th of the month can also be considered after taking necessary approvals.

Pre-EMI Charges are the different interest charges that a customer has to pay from the date of disbursement and the day of the start of the EMI.

Contact your Relationship Manager to take an informed decision for your case.

- Date of Disbursement is required

-

Date of Disbursement should be ideally within 7 working days before the registration date, as the validity of the cheque after disbursement is 7 working days.

After 7 days, the Bank is obliged to cancel the disbursement to protect the customer from unnecessary interest charges and the customer has to request his/her Relationship Manager for initiating the disbursement again basis the old disbursement.

Contact your Relationship Manager to take an informed decision for your case.

Contact your Relationship Manager for any process support

Visit Trackmyloan to know about the current status about your Loan.