Want us to help you with anything?

Request a Call back

Secure yourself from surging medical costs and unexpected health issues with the Health Top Up Policy. The Health Top Up Policy is a super top-up plan that extends your coverage for illnesses and expenses not covered by your base plan or top-ups, it also comes with a deductible threshold.

Above 21 years

- You can buy the Health Top-Up Insurance policy for yourself and your family members, children and parents.

For Children

- Child should be above 91 days in age and less than 21 years.

Age Proof

- Birth Certificate

- Passport

- 10th or 12th Standard Mark sheet

- Aadhaar Card

- Driver’s Licence

- Voter’s ID

- PAN Card etc.

Identity Proof

- Aadhaar Card

- Driver’s Licence

- Voter’s ID

- PAN Card

- Passport

Address Proof

- Aadhaar Card

- Telephone Bill

- Electricity Bill

- Passport

- Ration card

- Driver’s Licence

- Voter’s ID

- Passport sized photographs

- Medical Reports

Expenses related to any admission primarily for diagnostics and evaluation purposes only are excluded. Any diagnostic expenses which are not related or not incidental to the current diagnosis and treatment are excluded. |

Expenses related to any admission primarily for enforced bed rest and not for receiving treatment. This also includes: |

Obesity/ Weight Control: Expenses related to the surgical treatment of obesity that does not fulfil all the below conditions: |

Gender treatments: Expenses related to any treatment, including surgical management, to change characteristics of the body to those of the opposite sex. |

Hazardous or Adventure sports: Expenses related to any treatment necessitated due to participation as a professional in hazardous or adventure sports, including but not limited to, para-jumping, rock climbing, mountaineering, rafting, motor racing, horse racing or scuba diving, hand gliding, sky diving, deep-sea diving. |

Breach of law: Expenses for treatment directly arising from or consequent upon any Insured Person committing or attempting to commit a breach of law with criminal intent. |

Excluded Providers: Expenses incurred towards treatment in any hospital or by any Medical Practitioner or any other provider specifically excluded by the Insurer and disclosed in its website / notified to the policyholders are not admissible. However, in case of life threatening situations or following an accident, expenses up to the stage of stabilization are payable but not the complete claim. |

Circumcision whether or not necessitated by vaccination or inoculation or change of life or cosmetic or aesthetic treatment of any description, plastic surgery unless necessary for treatment of a disease not excluded by the terms of the policy or as may be necessitated due to treatment of an accident. |

Cosmetic or plastic Surgery: Expenses for cosmetic or plastic surgery or any treatment to change appearance unless for reconstruction following an Accident, Burn(s) or Cancer or as part of medically necessary treatment to remove a direct and immediate health risk to the insured. For this to be considered a medical necessity, It must be certified by the attending Medical Practitioner. |

Treatment for, alcoholism, drug or substance abuse or any addictive condition and consequences thereof. |

Treatments received in heath hydros, nature cure clinics, spas or similar establishments or private beds registered as a nursing home attached to such establishments or where admission is arranged wholly or partly for domestic reasons |

Dietary supplements and substances that can be purchased without prescription, including but not limited to Vitamins, minerals and organic substances unless prescribed by a medical practitioner as part of hospitalization claim or day care procedure. |

Expenses related to the treatment for correction of eye sight due to refractive error less than 7.5 dioptres. |

Expenses related to any unproven treatment, services and supplies for or in connection with any treatment. Unproven treatments are treatments, procedures or supplies that lack significant medical documentation to support their effectiveness |

Sterility and Infertility: Expenses related to sterility and infertility. This includes: |

The cost of spectacles and contact lenses, hearing aids. |

Dental treatment or surgery of any kind unless requiring hospitalisation. |

Convalescence, general debility, run-down condition or rest cure, congenital external disease or defects or anomalies, , intentional self-injury (whether arising from an attempt to suicide or otherwise) and use of intoxicating drugs and/or alcohol. |

Charges incurred at Hospital or Nursing Home primarily for diagnostic, X-Ray or laboratory examinations or other diagnostic studies not consistent with or incidental to the diagnosis and treatment of the positive existence or presence of any diseases, illness or injury whether or not requiring Hospitalisation/ Domiciliary Hospitalisation. |

Expenses on vitamins and tonics unless forming part of treatment for injury or disease as certified by the attending Medical Practitioner. |

Diseases, illness, accident or injuries directly or indirectly caused by or contributed to by nuclear weapons/materials or contributed to by or arising from ionising radiation or contamination by radioactivity by any nuclear fuel or from any nuclear waste or from the combustion of nuclear fuel. |

Voluntary medical termination of pregnancy during the first 12 weeks from the date of conception. |

Maternity: |

Naturopathy treatment |

Title |

Description |

Claim submission clause |

Claim must be filed within 30 days from the date of completion of treatment. However, the Company may at its absolute discretion consider waiver, of this Condition in extreme cases of hardship where it is proved to the satisfaction of the Company that under the circumstances in which the insured was placed it was not possible for him or any other person to give such notice or file claim within the prescribed time-limit. The claim would invite additional 10% co-payment over and above payable amount as per policy terms and conditions. |

Reasonable and Customary Charges |

Reasonable and Customary Charges will be applied on re-imbursement claims from non network hospitals where medical treatment taken by the Insured Person during the Policy Period following an Illness or Injury that occurs during the Policy Period, subject to availability of the Sum Insured and any specific limits specified in the Schedule of Benefits and the terms, conditions and exclusions specified in the Policy document. |

Claim Intimation & Network clause |

All Reimbursement Claims must be intimated to ILHC within 24 hrs of admission, in case of non intimation/ Delayed intimation 10% Co-pay would be applicable except for Accidental claims. If the member is getting admitted in any network hospital and filing for reimbursement claims such claims will be settled to members with 15% co-pay. |

Add-Del of Lives |

Premium to be charged as per fixed grid for addition endorsement. Premium to be refunded as per refund grid. No Refund for deletion if claim is under process or paid. |

Special Condition |

The Account holder (Proposer/ Applicant) to be one of the insured member in the policy |

Special Condition |

This policy only to be sourced along with the new salary/ savings account opening. |

Termination |

Policy will cease to be in effect from the date of termination of relationship with the organization. |

Only for the customers of ICICI Bank Ltd who intend to enroll under Health Shield 360 (Master policy no: 4177i/MSTR/291415383/00/000) underwritten by ICICI Lombard GIC Ltd. ICICI Bank Limited ("ICICI Bank") with registered office at ICICI Bank Tower, Near Chakli Circle, Old Padra Road, Vadodara, 390 007, Gujarat (CIN - L65190GJ1994PLC021012) is a Corporate Agent (Composite, IRDAI Regn. No.: CA0112) of ICICI Lombard General Insurance Company Limited (“ICICI Lombard”). Insurance is underwritten by ICICI Lombard.

Customer Support Email ID - customer.care@icicibank.com

ICICI Bank Ltd customer participation in the policy is entirely voluntary. This is only an indication of the cover offered for more details on risk factors, terms, conditions and exclusions, please read the sales brochure / policy wordings carefully before concluding a sale. ICICI trade logo displayed above belongs to ICICI Bank and is used by ICICI Lombard GIC Ltd. under license and Lombard logo belongs to ICICI Lombard GIC Ltd. ICICI Lombard General Insurance Company Limited, ICICI Lombard House, 414, Veer Savarkar Marg, Prabhadevi, Mumbai – 400025 Toll Free: 1800 2666 Fax No: 022 61961323 IRDA Reg. No. 115 CIN: L67200MH2000PLC129408 , ICICI Lombard Customer Support Email ID: customersupport@icicilombard.com Website Address: www.icicilombard.com Product Name: Health Shield 360. UIN: ICIHLGP22083V022122

BEWARE OF SPURIOUS PHONE CALLS AND FICTIOUS/FRADULENT OFFERS

IRDAI is not involved in activities like selling insurance policies, announcing bonus or investment of premiums.

Public receiving such phone calls are requested to lodge a police complaint.

Life Insurance

Trusted plans to secure your family

Guaranteed Pension Plan

A pension plan that ensures you enjoy financial freedom and live life on your own terms, even after retirement

Cancer Cover

Secure yourself against the risk of cancer

Travel Insurance

Travel Insurance provides utmost protection against unseen medical and non-medical emergencies.

Health Insurance

Premium starting at Rs 11 per day

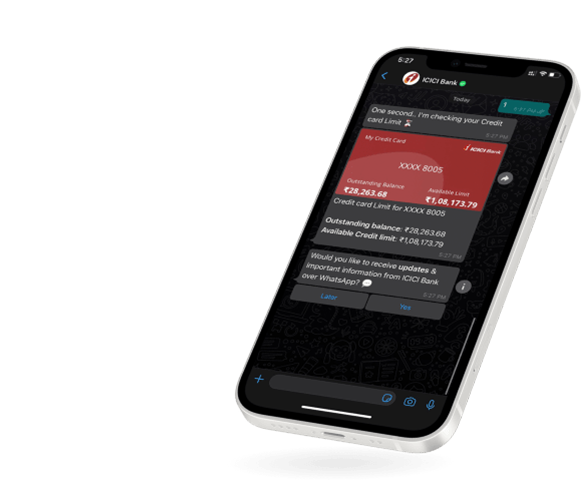

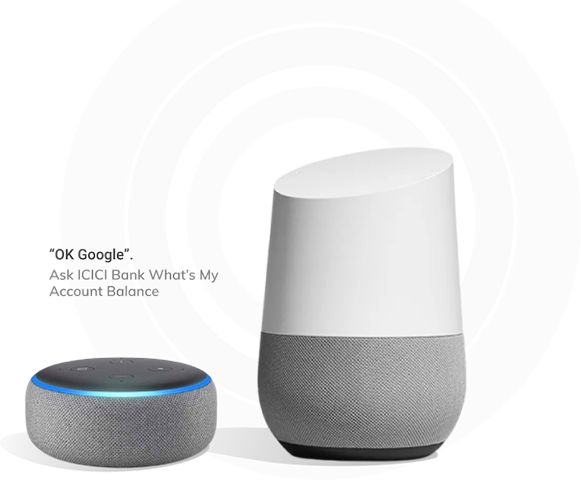

- Mobile Banking

- Net Banking

- WhatsApp Banking

- Voice Banking

Download

iMobile App

Click to Enlarge

Download

Pocket

Click to Enlarge

Quick tips and helpful product demonstration videos - ICICI Bank Online Demos & Videos

Explore NowScrollToTop