Apply Online

-

NRI Savings

-

NRE/NRO Savings

View NRE/NRO Savings

-

-

NRI Deposits

-

NRE/NRO FD & FCNR

Start using NRE/NRO FD & FCNR today!

-

-

.png)

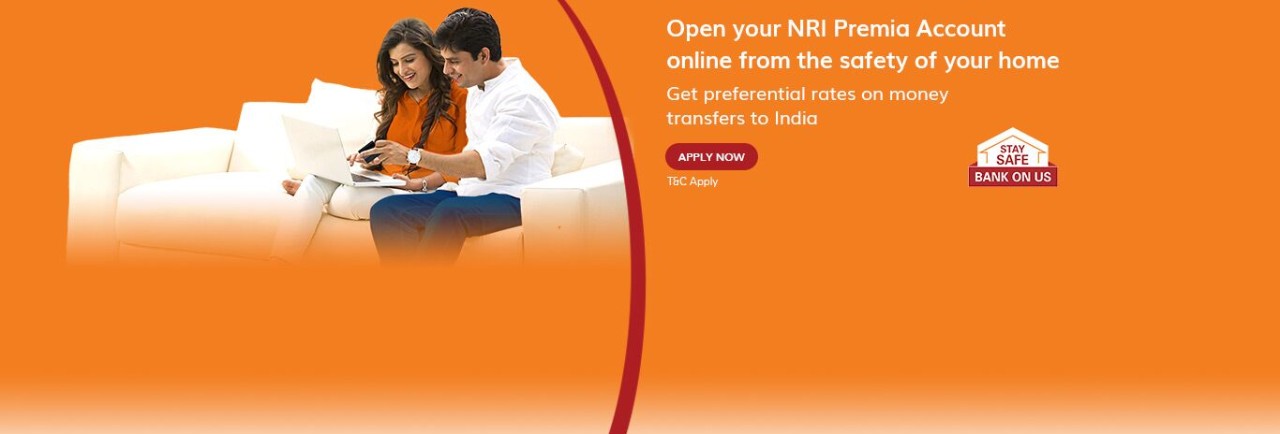

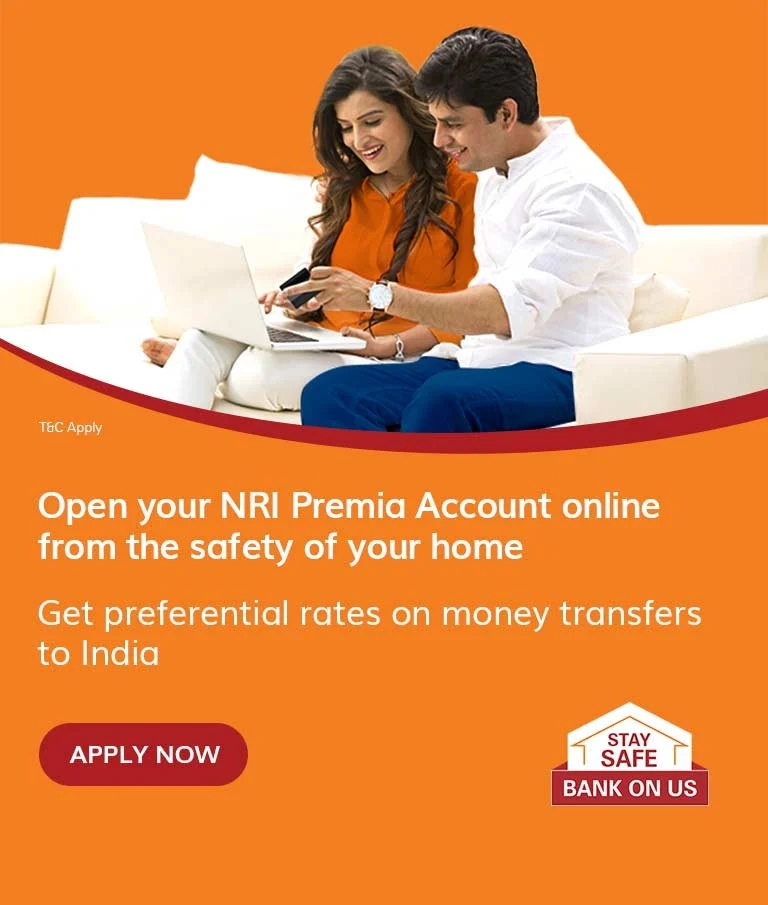

Premium Accounts

-

PRO/PREMIA Account

PRO/PREMIA Account Services

-

-

Student Account

-

Student Account

-

-

NRI Home Loan

-

NRI Home Loan

-

-

Global Accounts

-

Hello UK / Canada

-

Exchange Rates

Get in Touch

-

Service Channels

-

Service Channels

View Service Channels

-

-

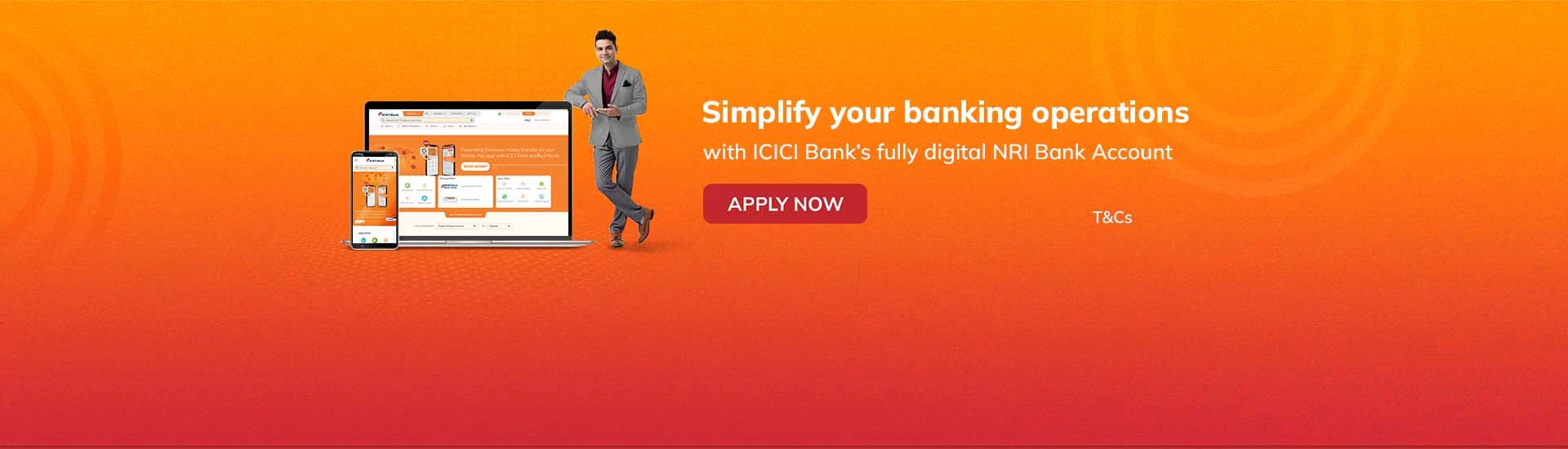

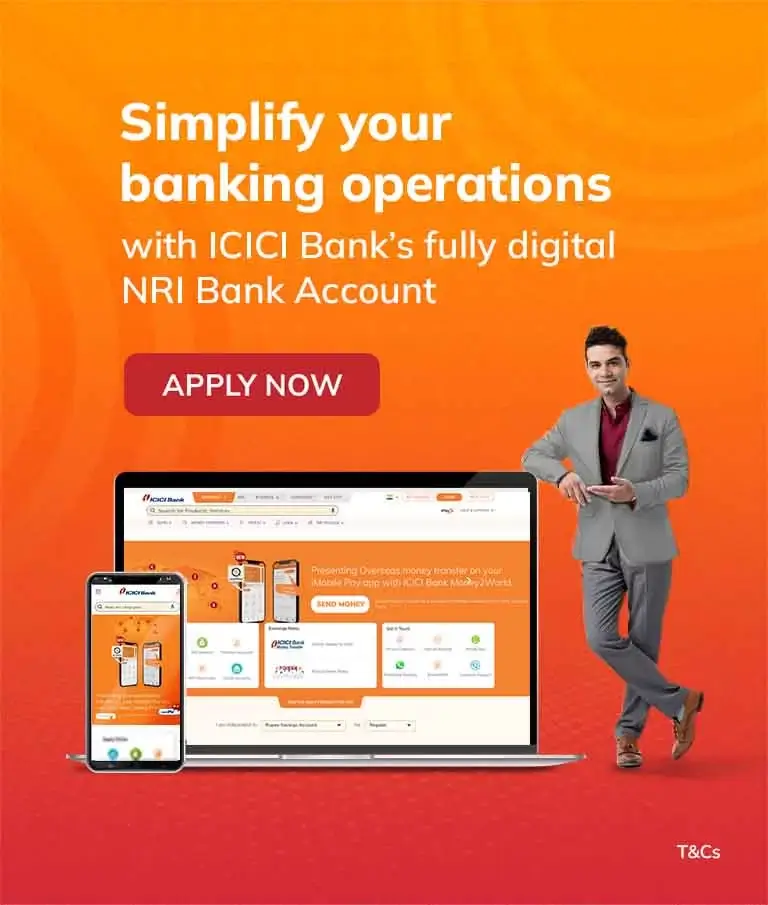

Internet Banking

-

Internet Banking

Start using your internet banking today!

-

-

Mobile App

-

Mobile App

NRI Mobile Banking

-

-

WhatsApp Banking

-

WhatsApp Banking

WhatsApp Banking-+91-8640086400

-

-

Branch/ATM

-

Branch/ATM

Branch Banking Services

-

-

Customer Support

-

Customer Support

Phone Banking Services

-

Wealth Plan

Dual benefit of protection along with returns on your savings

- Ensures that you receive a lumpsum amount of money at the maturity of the Policy.

- In the unfortunate event of death of the policyholder during the term of the policy, your family receives lumpsum amount, called the Sum Assured, as per applicable policy terms and conditions.

- Combines the benefits of protection and saving in a single instrument.

Retirement Plan

Your post retirement years to be financially secured and comfortable

- Ensures that you and your family members receive a regular pension amount post a retirement date.

- Flexibility to choose the retirement date and the manner in which you receive the pension.

- Combines the benefits of protection and saving in a single instrument.

Child Plan

Funds to fulfill various commitments in your child's educational milestones

- Ensures comprehensive financial planning for your child's education/ developmental needs.

- Flexibility in premium payment – Pay premium regularly or in a single lumpsum and you can withdraw money partially during the key educational milestones of your child.

- Offers financial protection to your child's future in the unfortunate event of death of the parent.

We take your security

seriously !

Peace of mind for you as we have the most advanced technology & protection

2 Factor i-safe authentication

End-to-end 256 bit Encryption

We make you feel special