Offers

Offers

Grow Investment

Grow Investment

Customer Care No.

Customer Care No.

Offers for you!!

.png)

Grow your Investment

For any banking assistance, please call our customer care number.

![]()

![]() 1800 1080

1800 1080

DIGITAL BANKING

Advance. Innovative. Instant

- Mobile Banking

- Net Banking

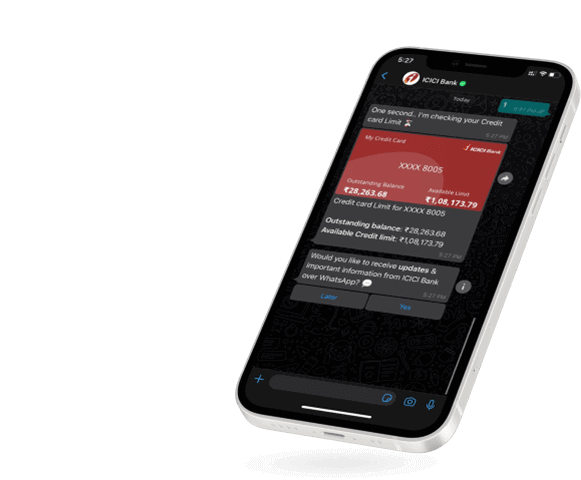

- WhatsApp Banking

DIGITAL BANKING

Advance. Innovative. Instant

Download

iMobile App

Click to Enlarge

Download

Pocket

Click to Enlarge

Exciting deals on ICICI Bank Net Banking

Explore now

We take your Banking security

seriously !

Peace of mind for you as we have the most advanced technology & protection

2 Factor i-safe authentication

End-to-end 256 bit Encryption

We make you feel special

Trending Deals

Great Offers for Great Experiences